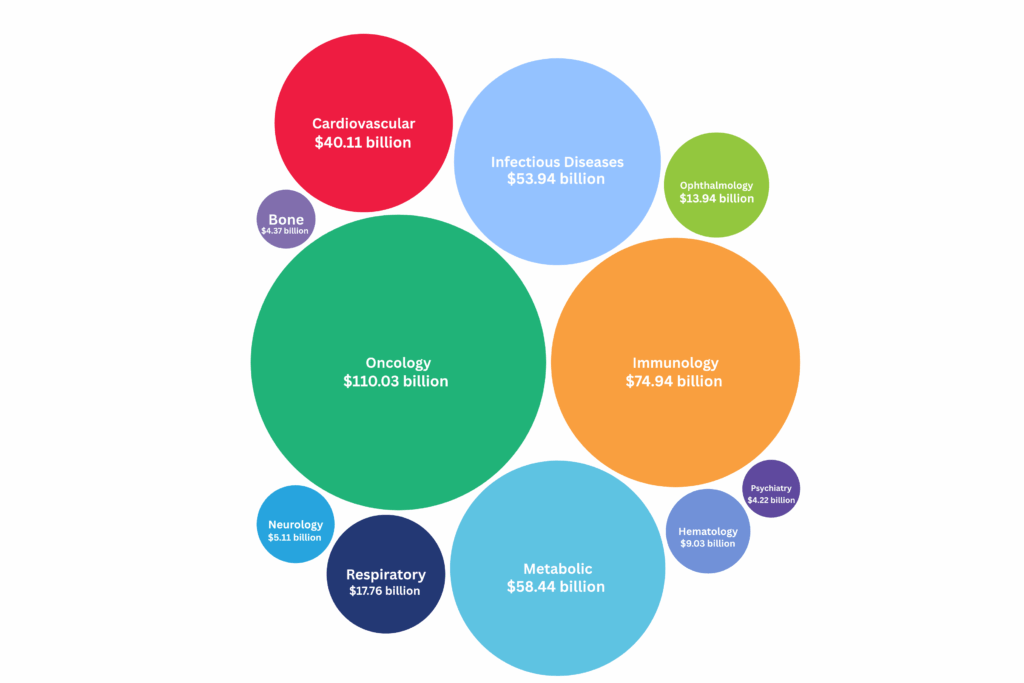

In 2024, the global pharmaceutical market witnessed unprecedented growth, with the top-selling drugs collectively generating over $116 billion in revenue.

Leading this surge was Merck’s immuno-oncology therapy, Keytruda, which maintained its position as the world’s best-selling drug with nearly $29.5 billion in sales. Following closely were Bristol Myers Squibb/Pfizer’s Eliquis, Novo Nordisk’s GLP-1 receptor agonist Ozempic and Sanofi/Regeneron’s Dupixent.

Immunology saw strong performances from Skyrizi (up 50.9% to $11.7 billion) and Dupixent (up 22.1%), while Humira declined 37.6% amid biosimilar pressure.

COVID-19 vaccine demand waned, with Comirnaty’s sales halving, though COVID antiviral Paxlovid rebounded with some growth.

Cardiometabolic and infectious disease treatments like Farxiga, the Jardiance family and Biktarvy also posted impressive gains.

Read more below to discover the top 50 best-selling drugs to watch in 2025, based on 2024’s sales data.

Data from https://www.drugdiscoverytrends.com/2024s-blockbusters-top-50-pharmaceuticals-by-sales/

When it comes to companies that report in foreign currencies, the conversion to US dollars uses the average annual exchange rates reported by the US Federal Reserve.

1. Keytruda (pembrolizumab)

Disease area(s): Oncology

Manufacturer(s): Merck

2024 Sales (USD): $29.48 billion

Why it sold so well: Merck’s flagship cancer immunotherapy Keytruda achieved expected, remarkable success in 2024, with global sales reaching $29.48 billion — an 18% increase from the previous year and accounting for 46% of the company’s total revenue. The growth was driven by expanded use in earlier-stage cancers, such as triple-negative breast cancer (TNBC), non-small cell lung cancer (NSCLC) and endometrial cancer, as well as sustained demand in metastatic indications. Merck also announced positive results from a pivotal Phase III trial of subcutaneous pembrolizumab combined with berahyaluronidase alfa, potentially enhancing patient convenience and expanding market reach. Merck has been actively working to secure Keytruda’s long-term market position by extending patent protections through supplementary certificates and pediatric exclusivity, potentially safeguarding its exclusivity until 2036 in the US. The company is facing some upcoming challenges, including anticipated government price negotiations and patent expirations around 2028.

2. Eliquis (apixaban)

Disease area(s): Cardiovascular/hematology

Manufacturer(s): Bristol Myers Squibb/Pfizer

2024 Sales (USD): $20.70 billion

Why it sold so well: Bristol Myers Squibb (BMS) and Pfizer’s jointly developed anticoagulant experienced robust performance in 2024, driven by strong demand and strategic positioning. BMS reported global Eliquis revenues of $13.33 billion, marking a 9% year-over-year increase, with US sales contributing $9.63 billion — a 14% rise attributed to higher demand and inventory build-up. It also noted that its 7% revenue increase was driven by the company’s growth portfolio and Eliquis. Pfizer also highlighted Eliquis as a key contributor to its 2024 financial results, accounting for 12% of the company’s revenue and serving as its top-selling product last year, having brought in $7.37 billion. Pfizer also noted Eliquis’ role in the company’s 7% year-over-year operational revenue growth. The sustained success of Eliquis is further supported by its patent protections, which have delayed generic competition in the US until at least 2026, and potentially until 2031. However, upcoming Medicare price negotiations under the Inflation Reduction Act (IRA) may impact future pricing and revenues for Eliquis.

3. Ozempic (semaglutide)

Disease area(s): Metabolic diseases

Manufacturer(s): Novo Nordisk

2024 Sales (USD): $17.45 billion

Why it sold so well: Novo Nordisk’s GLP-1 blockbuster for type 2 diabetes continued its impressive growth in 2024, with sales increasing by 26% year-over-year to DKK 120.3 billion ($17.45 billion). This surge was driven by strong demand in both North America and international markets, where Novo Nordisk leads in the GLP-1 diabetes segment and holds a 55.1% global value market share. The rising prevalence of diabetes worldwide and the expanding use of GLP-1 therapies contributed to Ozempic’s success. However, the rapid growth led to periodic supply constraints and drug shortage notifications across various regions, including the US. Analysts have projected Ozempic to become the world’s top-selling drug in a few years. But competition from Eli Lilly’s GLP-1 tirzepatide products, Mounjaro and Zepbound, could affect its growth. Additionally, the proliferation of compounded versions of semaglutide in the US impacted sales, prompting the FDA to set a deadline for pharmacies to cease their sale. Novo is investing in expanding its production capacity and developing next-generation obesity treatments, such as an oral version of semaglutide, to maintain its competitive edge in the rapidly growing GLP-1 market.

4. Dupixent (dupilumab)

Disease area(s): Immunology/respiratory

Manufacturer(s): Sanofi/Regeneron

2024 Sales (USD): $14.15 billion

Why it sold so well: Co-developed by Sanofi and Regeneron, Dupixent achieved significant success in 2024, with global net sales reaching $14.15 billion — a 22% increase over 2023. Sanofi reported that Dupixent sales exceeded €13.07 billion ($14.15 billion) for the year, driven by strong demand across multiple indications, including atopic dermatitis, asthma, chronic rhinosinusitis with nasal polyposis, eosinophilic esophagitis and prurigo nodularis. A major growth catalyst was the FDA approval of Dupixent as the first biologic treatment for chronic obstructive pulmonary disease (COPD) with an eosinophilic phenotype, opening a new market segment. Geographically, sales were robust in the US, Europe and emerging markets like China and Japan. Sanofi’s full-year revenue rose 8.6% to €41.08 billion, with Dupixent as a key contributor. Regeneron, which reported profits from Dupixent sales recorded by Sanofi, announced fourth-quarter revenues of $3.70 billion, surpassing expectations, and announced a new dividend and $3 billion share buyback program. Both companies anticipate continued growth for Dupixent, particularly as it gains traction in the COPD market and expands into additional indications.

5. Biktarvy (bictegravir/emtricitabine/tenofovir alafenamide)

Disease area(s): Infectious diseases (HIV)

Manufacturer(s): Gilead Sciences, Inc.

2024 Sales (USD): $13.42 billion

Why it sold so well: Gilead Sciences’ flagship HIV treatment, Biktarvy, had exceptional growth in 2024, with global sales increasing 13% year-over-year to $13.4 billion. The surge was primarily driven by heightened demand, favorable inventory dynamics and higher average realized prices. In the fourth quarter alone, Biktarvy’s sales rose 21% to $3.8 billion, reinforcing its position as the leading HIV regimen in the US and other major markets. The drug’s success significantly contributed to Gilead’s total HIV product sales, which reached $19.6 billion in 2024, an 8% increase over 2023. Biktarvy’s robust performance underscores Gilead’s effective lifecycle management and strategic market positioning within the HIV treatment landscape.

6. Jardiance family

Disease area(s): Metabolic/cardiovascular

Manufacturer(s): Boehringer Ingelheim/Eli Lilly and Company

2024 Sales (USD): $12.38 billion

Why it sold so well: Co-developed by Boehringer Ingelheim and Eli Lilly, the Jardiance family experienced robust growth in 2024, driven by expanding clinical indications and strong global demand. The Jardiance family includes several empagliflozin-based medications — Jardiance, Synjardy and Trijardy XR — used to manage type 2 diabetes, heart failure and chronic kidney disease. Boehringer reported that Jardiance generated €8.36 billion ($9.04 billion) in annual sales, marking a 13.2% increase over 2023. The growth was fueled by its efficacy in treating type 2 diabetes, heart failure and chronic kidney disease (CKD). In its annual report, Boehringer shared that Jardiance was the company’s best-selling product in 2024. Eli Lilly, which records Jardiance revenue as royalties, reported a 50% year-over-year increase in Q4 2024, reaching $1.2 billion. This surge included a one-time $300 million benefit from an amendment to its collaboration with Boehringer Ingelheim. In its 2024 annual report, Eli Lilly reported that Jardiance brought in $3.34 billion in annual sales, representing a 22% increase from 2023. The sustained success of Jardiance underscores the strategic value of the Boehringer-Lilly partnership and the drug’s expanding role in managing cardiometabolic diseases.

7. Skyrizi (risankizumab-rzaa)

Disease area(s): Immunology

Manufacturer(s): AbbVie

2024 Sales (USD): $11.72 billion

Why it sold so well: AbbVie’s IL-23 inhibitor Skyrizi had remarkable growth in 2024, with global net revenues hitting $11 billion — a 57.7% increase from 2023. The tremendous growth was driven by strong demand across multiple indications, including plaque psoriasis, psoriatic arthritis and Crohn’s disease. Notably, the FDA approved Skyrizi for ulcerative colitis in June 2024, further expanding its therapeutic reach. Skyrizi’s success significantly contributed to AbbVie’s immunology portfolio, which totaled $26.68 billion in 2024. The drug’s performance helped offset declining sales of Humira due to biosimilar competition. AbbVie projects combined sales of Skyrizi and Rinvoq to exceed $31 billion by 2027, underscoring Skyrizi’s role as a key growth driver for the company.

8. Darzalex (daratumumab) and Darzalex Faspro (daratumumab and hyaluronidase-fihj)

Disease area(s): Oncology/hematology

Manufacturer(s): Johnson & Johnson

2024 Sales (USD): $11.67 billion

Why it sold so well: Anti-CD38 monoclonal antibody Darzalex and its subcutaneous formulation, Darzalex Faspro, had exceptional success in 2024, becoming J&J’s top-selling pharmaceutical product with global net sales of $11.67 billion — a 19.8% increase over 2023. It accounted for about 13.1% of J&J’s total revenues in 2024. Its growth was driven by expanded adoption across multiple myeloma treatment regimens, including frontline and relapsed/refractory settings, as well as the convenience of the subcutaneous formulation, which reduces administration time and improved patient experience. In the fourth quarter alone, Darzalex generated over $3 billion in sales, marking the first time a single J&J drug surpassed that threshold in a quarter, the company said. In August 2024, the FDA approved Darzalex Faspro in combination with bortezomib, lenalidomide and dexamethasone for induction and consolidation in newly diagnosed multiple myeloma patients eligible for autologous stem cell transplant. Additionally, J&J submitted regulatory applications for Darzalex Faspro for high-risk smoldering multiple myeloma in both the US and the European Union (EU) in late 2024. Darzalex’s success could be further bolstered by positive clinical trial results, including the Phase III AQUILA study, which demonstrated that Darzalex Faspro significantly delayed progression from high-risk smoldering multiple myeloma to active disease and extended overall survival compared to active monitoring.

9. Mounjaro (tirzepatide)

Disease area(s): Metabolic diseases

Manufacturer(s): Eli Lilly and Company

2024 Sales (USD): $11.54 billion

Why it sold so well: Eli Lilly’s dual GIP and GLP-1 receptor agonist for type 2 diabetes, Mounjaro, experienced exceptional growth in 2024, with global sales more than doubling to $11.54 billion. This growth was driven by strong demand for its efficacy in glycemic control and weight loss. In the fourth quarter alone, Mounjaro’s sales increased 60% year-over-year to $3.53 billion, significantly contributing to Lilly’s record total quarterly revenue of $13.53 billion, a 45% increase over Q4 2023. The success of Mounjaro was bolstered by its expansion into new indications and markets, as well as increased manufacturing capacity to meet growing demand. The FDA removed Mounjaro and its obesity counterpart Zepbound from its drug shortages list in October 2024, which triggered backlash from compounders. Lilly’s strategic investments in production and supply chain enhancements ensured better product availability, supporting the drug’s rapid adoption. Lilly anticipates continued momentum for Mounjaro, projecting 2025 revenues between $58 billion and $61 billion, driven by Mounjaro and other key products. Following promising Phase III data showing Mounjaro’s benefits in heart failure with preserved ejection fraction in obese patients, Lilly submitted an FDA filing for the indication. It is also currently evaluating Mounjaro in a Phase II trial for MASH.

10. Stelara (ustekinumab)

Disease area(s): Immunology

Manufacturer(s): Johnson & Johnson

2024 Sales (USD): $10.36 billion

Why it sold so well: J&J’s immunology blockbuster Stelara generated approximately $10.36 billion in global sales in 2024, a 4.6% decline from the previous year. The decline was primarily due to biosimilar competition in Europe and the anticipation of biosimilar launches in the US in 2025, following patent settlements. Despite the drop, Stelara remained a significant revenue contributor, particularly in the US, where it achieved $6.72 billion in sales. As the company’s second-largest product with respect to sales, it accounted for approximately 11.7% of the company’s total revenues in 2024. Stelara’s continued success in 2024 was supported by its broad indications across inflammatory diseases, including Crohn’s disease, ulcerative colitis, plaque psoriasis and psoriatic arthritis. However, with the impending loss of exclusivity, J&J is focusing on newer therapies like Tremfya (guselkumab) to sustain growth in its immunology portfolio.

11. Trikafta/Kaftrio (elexacaftor/tezacaftor/ivacaftor)

Disease area(s): Respiratory/rare disease

Manufacturer(s): Vertex Pharmaceuticals Incorporated

2024 Sales (USD): $10.24 billion

Why it sold so well: Trikafta (marketed as Kaftrio outside the US), a combination therapy of elexacaftor, tezacaftor and ivacaftor, was the primary driver of Vertex Pharmaceuticals’ strong commercial performance in 2024. The company reported total product revenues of $11.02 billion for the year, a 12% increase from 2023, with Trikafta/Kaftrio accounting for the majority of sales. This growth was fueled by expanded global approvals and reimbursement agreements that improved patient access. By 2024, the therapy had been approved in over 60 countries, and Vertex secured favorable pricing and access deals, including a key agreement with the UK’s National Institute for Health and Care Excellence (NICE) that extended coverage to more patients. The drug’s widespread success is also rooted in its transformative clinical profile — Trikafta/Kaftrio is effective for about 90% of cystic fibrosis patients, including those with at least one F508del mutation, and has been shown to significantly improve lung function and quality of life. Its broad applicability and life-changing impact have made it the standard of care in many regions. Additionally, Vertex has leveraged its market exclusivity and maintained a high annual price — around $300,000 per patient in the US. The company is also investing in next-generation cystic fibrosis therapies such as the vanzacaftor triple combination (Alyftrek), which is expected to further reinforce its leadership in the cystic fibrosis space.

12. Eylea (aflibercept)

Disease area(s): Ophthalmology

Manufacturer(s): Regeneron/Bayer

2024 Sales (USD): $9.55 billion

Why it sold so well: Eylea registered strong sales in 2024, driven by the introduction of Eylea HD, which received FDA approval in 2023 and is an 8 mg formulation offering extended dosing intervals for retinal diseases. In the US, Regeneron reported combined Eylea and Eylea HD sales of $5.97 billion for the year, with Eylea HD contributing $1.2 billion. The higher-dose version saw significant uptake, accounting for over 10% of Bayer’s Eylea sales by year-end. Sales of Eylea reached €3.31 billion ($3.58 billion) last year. In its annual report for 2024, Bayer said it registered “encouraging sales growth” for Eylea in a number of areas, including Europe and Canada, “thanks to higher volumes and prices.” This growth was bolstered by Eylea HD for conditions like wet age-related macular degeneration (AMD), diabetic macular edema and diabetic retinopathy, allowing for more flexible dosing schedules. The launch of Eylea HD provided a boost to sales, especially in Japan and Europe, the company said. Despite emerging competition from biosimilars approved in 2024, Eylea maintained its market leadership, aided by strategic inventory management and the therapeutic advantages of its new formulation.

13. Opdivo (nivolumab)

Disease area(s): Oncology

Manufacturer(s): Bristol Myers Squibb

2024 Sales (USD): $9.30 billion

Why it sold so well: BMS’s flagship immunotherapy, Opdivo, achieved strong sales in 2024 due to several key factors. Global revenue reached $9.30 billion, a 3% year-over-year increase, driven by volume growth across multiple oncology indications. The FDA approved Opdivo Qvantig, a subcutaneous formulation of the drug, in early 2025, improving patient convenience and potentially expanding its market share. Additionally, the European Commission approved Opdivo plus Yervoy (ipilimumab) for first-line treatment of microsatellite instability-high or mismatch repair-deficient metastatic colorectal cancer, further broadening its therapeutic applications. These developments, coupled with Opdivo’s inclusion in BMS’s Growth Portfolio, which saw revenues increase by 17% to $22.56 billion, maintain its pivotal role in the company’s oncology strategy.

14. Humira (adalimumab)

Disease area(s): Immunology

Manufacturer(s): AbbVie

2024 Sales (USD): $8.99 billion

Why it sold so well: In 2024, Humira remained a significant revenue contributor for AbbVie, despite facing substantial declines due to biosimilar competition following its US loss of exclusivity in January 2023. Global Humira sales decreased by 37% year-over-year, totaling approximately $8.99 billion, with US revenues dropping 41% and international revenues declining 13%. The continued sales were supported by AbbVie’s strategic contracting and patient support programs, which helped retain a portion of the market share amidst the influx of biosimilars. The company’s robust immunology portfolio, including newer therapies like Skyrizi and Rinvoq, experienced significant growth, partially offsetting the decline in Humira sales.

15. Gardasil/Gardasil 9

Disease area(s): Vaccines/infectious diseases

Manufacturer(s): Merck

2024 Sales (USD): $8.58 billion

Why it sold so well: In 2024, Merck’s Gardasil/Gardasil 9 vaccine generated $8.58 billion in global sales, marking a 3% decline from the previous year, primarily due to reduced demand in China. Despite this downturn, the vaccine experienced double-digit sales growth in nearly every major region outside of China, particularly Japan, reflecting strong global demand. The decline in China was attributed to factors including decreased demand and an anti-corruption investigation targeting certain foreign companies, which has affected the medical products market. Merck announced it was pausing shipments to the country beginning in February 2025 through to at least mid-year to clear increasing inventory due to the decreased demand. Given this, Merck also decided to withdraw its $11 billion annual sales target for Gardasil by 2030. Nonetheless, Gardasil remains Merck’s second-largest revenue-generating product, underscoring its significance in the company’s portfolio. In January 2025, Merck also received expanded approval in China for Gardasil in males aged nine to 26 years. It is now the first HPV vaccine approved in China for the prevention of certain HPV-related cancers and diseases in males nine to 26 years of age.

16. Wegovy (semaglutide)

Disease area(s): Metabolic diseases

Manufacturer(s): Novo Nordisk

2024 Sales (USD): $8.44 billion

Why it sold so well: In 2024, Novo Nordisk’s obesity products, including Wegovy and Saxenda, achieved significant sales growth, increasing by 56% in Danish kroner to DKK 58.21 billion ($8.44 billion USD). This was driven by strong demand in both North America and international markets, reflecting the growing global prevalence of obesity and unrelenting demand for GLP-1-based treatments. To meet the demand, Novo has been investing in expanding its manufacturing capacity, including acquiring three Catalent manufacturing sites as part of its $16.5 billion acquisition of the company, completed in December 2024. Additionally, the company secured insurance coverage for Wegovy for approximately 55 million Americans, enhancing accessibility and contributing to its market leadership in obesity care.

17. Xtandi (enzalutamide)

Disease area(s): Oncology

Manufacturer(s): Astellas/Pfizer

2024 Sales (USD): $7.94 billion

Why it sold so well: In 2024, Astellas Pharma’s Xtandi, co-marketed with Pfizer, posted strong sales growth, with revenues reaching ¥703.1 billion ($4.64 billion) for the first nine months (April 1, 2024 to December 31, 2024), marking a 25.6% increase compared to the same period in the previous year. The robust performance was primarily driven by strong demand in the US, where sales rose by 38.2%, fueled by the drug’s penetration into the non-metastatic castration-sensitive prostate cancer (M0 CSPC) segment and its established use in other indications, the company said. The expansion of Xtandi’s indications and its continued efficacy contributed to its strong market presence. Pfizer’s revenue from Xtandi reached approximately $565 million in the fourth quarter, reflecting a 24% year-over-year increase and totaled $2.04 billion for the year, accounting for approximately 3% of the company’s total revenue, reflecting a significant increase from the previous year’s revenue of $1.66 billion. The growth was driven by expanded usage in M0 CSPC as well as continued strong performance in metastatic castration-resistant prostate cancer (mCRPC). The drug’s robust demand contributed to Pfizer’s oncology portfolio growth, which saw a 30% increase in sales during the same period.

18. Entresto (sacubitril/valsartan)

Disease area(s): Cardiovascular

Manufacturer(s): Novartis

2024 Sales (USD): $7.82 billion

Why it sold so well: In 2024, Novartis’ heart failure medication, Entresto, had remarkable sales growth, generating $7.8 billion in revenue, a 31% increase over the previous year. This surge was driven by robust demand in both the US and international markets, with US sales growing by 41% and ex-US sales by 26% in constant currencies. The drug’s efficacy in treating heart failure with reduced ejection fraction (HFrEF) and its expanding adoption in hypertension management, particularly in China and Japan, contributed to its strong performance. Entresto had a balanced global sales distribution — approximately 50% in the US, 20% in Europe, 10% in China and 5% in Japan. Looking ahead, Novartis anticipates potential generic competition in the US by mid-2025 but expects continued growth in other regions due to extended regulatory data protection and possible additional exclusivity.

19. Comirnaty (tozinameran)

Disease area(s): Vaccines/infectious diseases

Manufacturer(s): Pfizer/BioNTech

2024 Sales (USD): $7.79 billion

Why it sold so well: In 2024, Pfizer’s COVID-19 vaccine, Comirnaty, generated $3.38 billion in revenue during the fourth quarter, surpassing expectations by approximately $280 million, and $5.35 billion for the year. This performance was attributed to stronger-than-anticipated demand, particularly in the US, as the vaccine transitioned to a commercial market model. Despite a 38% year-over-year decline in fourth-quarter sales and 53% drop in annual sales compared to the previous year due to reduced global vaccination rates and fewer contracted doses, Comirnaty remained one of Pfizer’s top-selling products for the year. For BioNTech, the company reported total revenues of €2.75 billion ($2.98 billion), a 27% decrease from the previous year, primarily due to reduced demand for its Comirnaty, the company’s only commercial product. The decline was further impacted by inventory write-downs and decreased gross profit share from its collaboration with Pfizer. These factors contributed to BioNTech’s first annual net loss since 2019. The German biotech is currently advancing its oncology pipeline, which includes more than 20 active Phase II and Phase III trials with a focus on two priority pan-tumor programs that includes mRNA cancer immunotherapies.

20. Farxiga/Forxiga (dapagliflozin)

Disease area(s): Metabolic diseases

Manufacturer(s): AstraZeneca

2024 Sales (USD): $7.72 billion

Why it sold so well: In 2024, AstraZeneca’s Farxiga achieved robust sales growth, with revenues increasing by 21% year-over-year to $1.9 billion in the fourth quarter alone and by 28% compared to 2023, making it the company’s top seller in 2024. This performance was driven by strong demand across its approved indications, including type 2 diabetes, heart failure and chronic kidney disease. The drug’s broad therapeutic utility and expansion into new markets contributed to its success. Additionally, Farxiga was among the medications selected for Medicare price negotiations under the Inflation Reduction Act, with the negotiated price set to take effect in 2026. Despite the anticipated price reductions, AstraZeneca has expressed confidence in Farxiga’s continued growth trajectory.

21. Ocrevus (ocrelizumab)

Disease area(s): Neurology/immunology

Manufacturer(s): Roche

2024 Sales (USD): $7.66 billion

Why it sold so well: In 2024, Roche’s multiple sclerosis (MS) therapy Ocrevus achieved sales of CHF 6.74 billion ($7.66 billion), marking a 9% increase from the previous year. This growth was driven by continued demand across both relapsing and primary progressive MS indications, particularly in the US, where sales rose by 5%, and in Europe, with a 14% increase, notably in the UK and Germany. The introduction of a subcutaneous formulation, approved in September 2023, offered patients a more convenient administration option compared to the traditional intravenous infusion, enhancing its competitiveness against similar therapies like Novartis’ Kesimpta. Additionally, Ocrevus’ strong performance in international markets, including a 29% sales increase, contributed to its position as Roche’s highest-selling medicine in the Pharmaceuticals Division.

22. Tagrisso (osimertinib)

Disease area(s): Oncology

Manufacturer(s): AstraZeneca

2024 Sales (USD): $6.58 billion

Why it sold so well: In 2024, AstraZeneca’s EGFR-TKI Tagrisso registered $6.58 billion in global sales, reflecting a 13% year-over-year increase. This growth was propelled by significant regulatory approvals, including the FDA’s endorsement of Tagrisso combined with chemotherapy for first-line treatment of EGFR-mutated non-small cell lung cancer (NSCLC) and its use in unresectable stage III NSCLC following chemoradiation therapy. These approvals expanded Tagrisso’s applicability across various stages of lung cancer. AstraZeneca also shared positive trial results for immunotherapy Imfinzi (durvalumab) and Tagrisso, which were “unprecedented in lung cancer,” the company said. Robust demand in key markets such as the US, Europe and China further contributed to its strong performance.

23. Prevnar family (pneumococcal 13-valent conjugate vaccine)

Disease area(s): Vaccines/infectious diseases

Manufacturer(s): Pfizer

2024 Sales (USD): $6.41 billion

Why it sold so well: In 2024, Pfizer’s Prevnar family of pneumococcal vaccines generated $6.4 billion in global revenue, accounting for 10% of the company’s total revenue and ranking as its second-highest-selling product after Eliquis. The strong performance was primarily driven by increased demand for pediatric vaccinations in the US, attributed to favorable timing of government purchases and higher patient demand in the private market. Additionally, there was strong uptake of the adult indication in certain international markets, contributing to the overall growth. Despite a decline in adult vaccinations in the US, the Prevnar franchise’s broad immunization coverage and established reputation for safety and efficacy supported its continued success. Pfizer’s strategic focus on expanding access to pneumococcal vaccines globally further reinforced Prevnar’s position as a cornerstone of its vaccine portfolio.

24. Imbruvica (ibrutinib)

Disease area(s): Oncology/hematology

Manufacturer(s): AbbVie/Johnson & Johnson

2024 Sales (USD): $6.39 billion

Why it sold so well: In 2024, Johnson & Johnson saw a 7% decline in global revenues of Imbruvica, primarily due to decreased demand and lower market share in the US, as well as reduced collaboration revenues internationally. Despite these challenges, the drug maintained its position as a key therapy for certain blood cancers. However, the emergence of newer treatments and increased competition have impacted its sales performance. Looking ahead, Imbruvica is expected to face additional pricing pressures, particularly under Medicare negotiations set to take effect in 2026. At the same time, J&J has submitted an application to the European Medicines Agency (EMA) requesting approval for a new indication for Imbruvica in adults with previously untreated mantle cell lymphoma (MCL) who are eligible for autologous stem cell transplantation.

25. Cosentyx (secukinumab)

Disease area(s): Immunology

Manufacturer(s): Novartis

2024 Sales (USD): $6.14 billion

Why it sold so well: In 2024, Novartis’ Cosentyx registered significant sales growth, with revenues increasing by 23% year-over-year to $6.14 billion. This performance was driven by strong demand across the US, Europe and emerging markets, fueled by recent launches, including the hidradenitis suppurativa (HS) indication and the intravenous formulation in the US. Additionally, volume growth in core indications such as psoriasis, psoriatic arthritis (PsA), ankylosing spondylitis (AS) and non-radiographic axial spondyloarthritis (nr-axSpA) contributed to the robust sales. Novartis said Cosentyx’s sustained efficacy and safety profile, with over 1.7 million patients treated across eight indications since its initial approval in 2015, further supported its market performance. The drug’s success played a pivotal role in Novartis raising its 2024 earnings guidance for the third time.

26. Xarelto (rivaroxaban)

Disease area(s): Cardiovascular/hematology

Manufacturer(s): Bayer/Johnson & Johnson

2024 Sales (USD): $6.14 billion

Why it sold so well: In 2024, Bayer’s Xarelto experienced a significant 7% decline in global revenues of Imbruvica due to the expiration of its patent protection, leading to increased generic competition. The loss of exclusivity resulted in a marked decrease in revenue for the drug, as highlighted in Bayer’s financial reports. The company anticipated the downturn, noting that the impact of the Xarelto patent loss would accelerate, affecting net sales and profit margins. Consequently, Bayer projected that its Pharmaceuticals division would face challenges in maintaining previous sales levels, with expectations of net sales slightly below those of 2024.

27. Rinvoq (upadacitinib)

Disease area(s): Immunology

Manufacturer(s): AbbVie

2024 Sales (USD): $5.97 billion

Why it sold so well: AbbVie’s Rinvoq experienced substantial sales growth in 2024, with global revenues increasing by 46.2% year-over-year to $1.83 billion in the fourth quarter alone. The growth was driven by strong demand across multiple immunological indications, including rheumatoid arthritis, psoriatic arthritis and ulcerative colitis. Rinvoq’s performance was further bolstered by its strategic positioning to offset declining Humira sales due to biosimilar competition. The drug’s success contributed to AbbVie’s decision to raise its full-year adjusted earnings guidance, reflecting confidence in Rinvoq’s continued growth trajectory. Analysts project that, combined with Skyrizi, Rinvoq’s sales could exceed $31 billion by 2027, underscoring its significance in AbbVie’s immunology portfolio.

28. Entyvio (vedolizumab)

Disease area(s): Immunology

Manufacturer(s): Takeda

2024 Sales (USD): $5.81 billion

Why it sold so well: Last year marked 10 years since the drug was first approved in 2014. Entyvio’s performance last year was primarily driven by the successful launch of the Entyvio Pen for subcutaneous administration in the US, which touts to enhance patient convenience and adherence. The introduction of the subcutaneous formulation contributed to Entyvio maintaining its position as the leading treatment in the inflammatory bowel disease (IBD) market in the US.

29. Revlimid (lenalidomide)

Disease area(s): Oncology/hematology

Manufacturer(s): Bristol Myers Squibb

2024 Sales (USD): $5.77 billion

Why it sold so well: In 2024, BMS’ Revlimid generated $5.77 billion in global revenue, maintaining its position as one of the company’s top-selling products despite facing generic competition. Its performance was bolstered by sustained demand in certain international markets and the continued clinical utility of Revlimid in treating multiple myeloma and other hematologic malignancies. While the company experienced revenue declines in its Legacy Portfolio due to generic erosion, Revlimid’s sales remained resilient, contributing significantly to BMS’ overall financial results.

30. Paxlovid (nirmatrelvir/ritonavir)

Disease area(s): Infectious diseases (antivirals)

Manufacturer(s): Pfizer

2024 Sales (USD): $5.72 billion

Why it sold so well: In 2024, Pfizer’s COVID-19 antiviral treatment, Paxlovid, generated $5.72 billion in global revenue, making it the company’s third-highest-selling product for the year. Its strong performance was primarily driven by the transition to commercial market sales in the US, including a $771 million favorable adjustment related to returned government stock. Additionally, Pfizer fulfilled its obligation to deliver 1 million treatment courses to the US Strategic National Stockpile, contributing $442 million to Paxlovid’s revenue. The continued demand for effective COVID-19 treatments, particularly among high-risk populations, supported Paxlovid’s robust sales. However, analysts anticipate a decline in Paxlovid sales in 2025 due to a smaller US winter COVID wave and reduced government purchases.

31. Vyndaqel (tafamidis)

Disease area(s): Cardiovascular/Rare disease

Manufacturer(s): Pfizer

2024 Sales (USD): $5.45 billion

Why it sold so well: In 2024, Pfizer’s Vyndaqel family (including Vyndaqel, Vyndamax and Vynmac) achieved significant sales growth, with global revenues increasing by 60% year-over-year. The surge was driven by heightened demand, particularly in the US and developed international markets, attributed to improved diagnosis rates of transthyretin amyloid cardiomyopathy (ATTR-CM) and enhanced affordability in the US. Vyndaqel ranked among Pfizer’s top 10 medicines and vaccines by revenue in 2024. The drug’s strong performance contributed to Pfizer’s overall 12% operational revenue growth in its non-COVID product portfolio for the year.

32. Verzenio (abemaciclib)

Disease area(s): Oncology

Manufacturer(s): Eli Lilly and Company

2024 Sales (USD): $5.31 billion

Why it sold so well: In 2024, Eli Lilly’s treatment for HR-positive, HER2-negative breast cancer, Verzenio, experienced substantial sales growth, with global revenues increasing by 36% year-over-year to $1.56 billion in the fourth quarter, and $5.31 billion for the full year, an increase of 37% from the previous year. The robust growth was driven by expanded use in both early and advanced breast cancer settings, particularly following its approval for adjuvant treatment in high-risk early-stage patients. The drug’s strong performance contributed to Lilly’s overall revenue growth of 45% in the fourth quarter.

33. Trulicity (dulaglutide)

Disease area(s): Metabolic diseases

Manufacturer(s): Eli Lilly and Company

2024 Sales (USD): $5.25 billion

Why it sold so well: In 2024, Eli Lilly’s Trulicity experienced a decline in sales, primarily due to increased competition and market dynamics. In the fourth quarter, global revenue for Trulicity decreased by 26% year-over-year to $1.25 billion and ended the year with $5.25 billion, down from $7.13 billion in 2023. The downturn was attributed to the growing presence of newer GLP-1 receptor agonists, such as Lilly’s own trizepatide products Mounjaro and Zepbound, which have shown greater efficacy in glycemic control and weight loss. Despite the decline, Trulicity remained a significant contributor to Lilly’s diabetes portfolio, despite its market share facing pressure from emerging treatments. Mounjaro, Trulicity and Zepbound accounted for 48% of Lilly’s total revenues in 2024. Lilly is also bracing itself for Trulicity to lose key patent and data exclusivity protections in the coming years.

34. Hemlibra (emicizumab)

Disease area(s): Hematology

Manufacturer(s): Roche

2024 Sales (USD): $5.11 billion

Why it sold so well: In 2024, global sales of Roche’s Hemlibra totaled $5.11 billion, marking a 9% increase over the previous year. Roche said the growth was partly attributed to temporary inventory stocking by US distributors in the final quarter of the year. In Europe, Hemlibra sales increased by 11%, driven by expanded market penetration, particularly in the non-inhibitor indication in countries like France and the UK. The drug’s continued adoption across various regions underscores its growing role in the treatment of hemophilia A. Hemlibra was also highlighted as one of Roche’s top five growth drivers in 2024.

35. Lynparza (olaparib)

Disease area(s): Oncology

Manufacturer(s): AstraZeneca/Merck

2024 Sales (USD): $4.98 billion

Why it sold so well: AstraZeneca’s Lynparza delivered a strong sales performance in 2024, with product revenues reaching $3.67 billion, marking a 22% increase at constant exchange rates compared to the previous year. AstraZeneca highlighted that the figure includes a $600 million sales-related milestone receivable from Merck. Similarly, Merck’s alliance revenue from Lynparza totaled $1.31 billion in 2024, up from 2023’s $1.20 billion. The performance was driven by expanded indications, including approvals in prostate, pancreatic and HER2-negative breast cancers, and strong uptake in ovarian cancer treatments. Lynparza’s sustained efficacy and safety profile, supported by ongoing clinical trials that supported broader reimbursement and adoption, bolster its position in the oncology market. The integrated co-commercialization efforts by AstraZeneca and Merck enabled effective market penetration and optimized distribution across key geographies. These factors not only enhanced its competitive positioning as a leading PARP inhibitor but also contributed significantly to the robust growth of both companies’ oncology portfolios.

36. Jakafi (ruxolitinib)

Indication(s): Intermediate‑ or high‑risk myelofibrosis, polycythemia vera (after hydroxyurea failure), acute graft‑versus‑host disease (GVHD) and chronic GVHD in adults (and pediatric patients 12 years and older)

Manufacturer(s): Incyte (in the US)/Novartis

2024 Sales: $4.73 billion

Why it sold so well: Jakafi generated approximately $2.8 billion in sales in 2024, marking a solid 8% YoY increase. The drug saw especially strong performance in Q4, with sales rising 11% to around $773 million. Outside the US, Novartis brought in $1.9 billion from Jakafi sales. Its broad utility in hematologic malignancies and post-transplant complications, along with steady payer demand, has cemented Jakafi as a cornerstone JAK-STAT inhibitor, delivering reliable growth despite increasing competition. As US patent exclusivity approaches its 2028 expiration, key dynamics to watch include potential label expansions (such as additional GVHD or inflammatory indications), intensifying competition from next-generation JAK inhibitors and Incyte’s ability to sustain patient demand while adapting to pricing reforms. The company has raised its 2024 sales forecast to between $2.74 billion and $2.77 billion, driven by strong uptake in polycythemia vera and GVHD.

37. Imfinzi (durvalumab)

Disease area(s): Oncology

Manufacturer(s): AstraZeneca

2024 Sales (USD): $4.72 billion

Why it sold so well: In 2024, AstraZeneca’s Imfinzi experienced strong sales growth, driven by expanded indications and robust clinical trial results. Its 2024 global sales amounted to $4.72 billion, a 17.44% increase from the previous year. In the first quarter of 2024, Imfinzi generated $1.26 billion in sales, making it AstraZeneca’s second-biggest cancer drug. Overall, AstraZeneca’s oncology segment, which includes Imfinzi, reported a 21% increase in total revenue for the year, driven by company blockbusters Tagrisso, Lynparza, Calquence, Imfinzi and Enhertu. Notably, the NIAGARA trial showed that the immunotherapy can significantly prolong survival in bladder cancer patients, while the ADRIATIC study marked the first and only immuno-oncology trial to demonstrate a survival benefit in limited-stage small cell lung cancer.

38. Xolair (omalizumab)

Disease area(s): Immunology/respiratory

Manufacturer(s): Roche/Novartis

2024 Sales (USD): $4.45 billion

Why it sold so well: Roche’s asthma drug Xolair clocked in global sales of CHF 2.47 billion ($2.80 billion) in 2024, marking a 16% increase compared to the previous year. This robust growth was primarily driven by strong demand in the US, reflecting the drug’s continued success in treating allergic asthma and chronic spontaneous urticaria. Additionally, the expansion into new indications, such as food allergies, contributed to the increased uptake. Roche’s US sales increased by 9%, driven largely by eye drug Vabysmo, MS drug Ocrevus, Xolair and Polivy. Novartis is responsible for marketing Xolair and recording all sales and related costs outside the US. For the full year 2024, Novartis reported net sales of Xolair totaling $1.64 billion, reflecting a 15% increase in constant currencies.

39. Vabysmo (faricimab)

Disease area(s): Ophthalmology

Manufacturer(s): Roche

2024 Sales (USD): $4.39 billion

Why it sold so well: In 2024, Roche’s Vabysmo had remarkable commercial success, with global sales reaching $4.39 billion, representing a 68% increase at constant exchange rates compared to the previous year. This growth was driven by strong demand across all regions, particularly in the US, where sales amounted to $3.29 billion, reflecting a 57% increase. Roche’s company sales grew by 10%, driven primarily by the continued growth of Vabysmo. Vabysmo’s unique dual-targeting mechanism, addressing both VEGF-A and Ang-2 pathways, contributed to its rapid adoption in treating neovascular age-related macular degeneration (nAMD) and diabetic macular edema (DME). Roche said Vabysmo showed a high uptake among both newly diagnosed patients as well as patients transitioning from other treatment options. Vabysmo prefilled syringe (PFS) was approved in the European Union (EU) for nAMD, DME and retinal vein occlusion (RVO). It is the first and only bispecific antibody available in a PFS, providing a more convenient option than the standard vial.

40. Prolia (denosumab)

Disease area(s): Bone health

Manufacturer(s): Amgen

2024 Sales (USD): $4.37 billion

Why it sold so well: In 2024, Amgen’s Prolia achieved strong sales, with global revenues increasing by 8% year-over-year to $4.37 billion for the year, driven primarily by volume growth. The osteoporosis drug accounted for 14% of Amgen’s total product sales last year. The performance reflects Prolia’s continued leadership in the osteoporosis market. In the US, it is primarily used for the treatment of postmenopausal women with osteoporosis at high risk of fracture and for treatment to increase bone mass in men with osteoporosis at high risk of fracture. Amgen anticipates potential sales erosion in 2025 due to biosimilar competition, particularly in the second half of the year. In the US, Prolia’s patent expired in February 2025, while in certain European countries, it will expire in November 2025.

41. Ibrance (palbociclib)

Disease area(s): Oncology

Manufacturer(s): Pfizer

2024 Sales (USD): $4.37 billion

Why it sold so well: Pfizer’s Ibrance generated $4.37 billion in global revenue in 2024, maintaining its position as a leading therapy for hormone receptor-positive (HR+), HER2-negative metastatic breast cancer. Ibrance was Pfizer’s sixth best-selling medicine last year. The drug’s continued adoption was bolstered by positive results from the Phase III PATINA trial, which demonstrated that adding Ibrance to standard anti-HER2 and endocrine therapy extended median progression-free survival by over 15 months in patients with HR+, HER2-positive metastatic breast cancer. This marked the first time a CDK4/6 inhibitor showed benefit in this patient population. Despite facing pricing pressures and generic competition in certain international markets, Ibrance’s strong clinical profile and expanded indications contributed to its solid performance in 2024.

42. Shingrix (herpes zoster vaccine)

Disease area(s): Vaccines/infectious diseases

Manufacturer(s): GSK

2024 Sales (USD): $4.30 billion

Why it sold so well: GSK’s shingles vaccine Shingrix achieved global sales of £3.36 billion ($4.30 billion), reflecting a 1% increase at constant exchange rates compared to the previous year. This growth was primarily driven by strong international demand, particularly in Europe and Australia, where expanded public funding and national immunization programs boosted uptake. Notably, markets outside the US accounted for 56% of Shingrix’s global sales in 2024, up from 45% in 2023, as the vaccine was launched in 52 countries. In the US, sales declined by 18% due to a slowing pace of reaching unvaccinated populations and changes in pharmacy reimbursement processes under new CMS rules. GSK is also evaluating the safety and efficacy of co-administering Shingrix with seasonal flu vaccines, including the company’s RSV vaccine, Arexvy. Building on 2023 data showing compatibility with seasonal flu vaccines, GSK presented 2024 results confirming that Arexvy can also be given alongside Shingrix, with additional co-administration trials, including with pneumococcal vaccines, currently underway.

43. Invega Sustenna/Xeplion/Invega Trinza/Trevicta (paliperidone)

Disease area(s): Psychiatry

Manufacturer(s): Johnson & Johnson

2024 Sales (USD): $4.22 billion

Why it sold so well: In 2024, J&J’s long-acting antipsychotic portfolio —including Invega Sustenna, Xeplion, Invega Trinza and Trevicta — registered global sales of $4.22 billion, reflecting a 2.6% year-over-year increase. This growth was primarily driven by a 7.9% increase in US sales, reaching $3.13 billion, while international sales declined by 9.9% to $1.10 billion, influenced by currency fluctuations and market dynamics. The portfolio’s performance underscores its continued importance in the treatment of schizophrenia and schizoaffective disorder, offering patients the benefits of long-acting injectable formulations. These therapies contribute significantly to J&J’s neuroscience segment, which reported total revenues of $7.12 billion in 2024.

44. Tecentriq (atezolizumab)

Disease area(s): Oncology

Manufacturer(s): Roche

2024 Sales (USD): $4.13 billion

Why it sold so well: In 2024, Roche’s cancer immunotherapy Tecentriq posted global sales of CHF 3.64 billion ($4.13 billion) and was the company’s fourth best-selling drug after MS drug Ocrevus, hemophilia treatment Hemlibra and eye drug Vabysmo. This growth was primarily driven by strong demand in Europe and internationally, where sales increased by 10% and 32%, respectively. However, US sales declined by 8% due to intensified competition in key indications, such as non-small cell lung cancer (NSCLC) and hepatocellular carcinoma (HCC). Despite these challenges, Tecentriq maintained its position as a significant contributor to Roche’s oncology portfolio, benefiting from its broad range of approved indications and ongoing clinical development programs.

45. Perjeta (pertuzumab)

Disease area(s): Oncology

Manufacturer(s): Roche

2024 Sales (USD): $4.11 billion

Why it sold so well: Roche’s Perjeta generated global sales of CHF 3.62 billion ($4.11 billion) last year, maintaining its position as a key therapy in HER2-positive breast cancer. While overall sales remained stable, the drug faced regional shifts. In Europe, sales declined due to the ongoing conversion of patients to Phesgo, a subcutaneous combination of Perjeta and Herceptin. Conversely, internationally, Perjeta experienced continued growth, partly because Phesgo had not yet been launched or reimbursed in some major markets, resulting in a relatively lower impact from patient conversion. Additionally, sales in China increased by 14%, driven by sustained demand for Perjeta and other oncology products. Perjeta ranked as Roche’s fifth best-selling drug in 2024.

46. Ofev (nintedanib)

Disease area(s): Respiratory

Manufacturer(s): Boehringer Ingelheim

2024 Sales (USD): $4.07 billion

Why it sold so well: In 2024, Boehringer Ingelheim’s Ofev achieved significant commercial success, with global sales reaching €3.77 billion ($4.07 billion), marking a 7.3% increase at constant exchange rates compared to the previous year. This growth was driven by the drug’s continued efficacy in treating idiopathic pulmonary fibrosis (IPF) and other fibrosing interstitial lung diseases (ILDs), solidifying its position as a leading therapy in the respiratory disease market. Boehringer’s sustained investment in research and development, including the advancement of new treatments like nerandomilast for progressive pulmonary fibrosis, further reinforced Ofev’s market presence. Boehringer’s sales were up 6.1% in 2024, led by diabetes medicine Jardiance along with Ofev.

47. Ultomiris (ravulizumab-cwvz)

Indication(s): Multiple rare, complement-mediated disorders, including paroxysmal nocturnal hemoglobinuria (PNH), atypical hemolytic uremic syndrome (aHUS), generalized myasthenia gravis (gMG), neuromyelitis optica spectrum disorder (NMOSD)

Manufacturer(s): Alexion/AstraZeneca

2024 Sales: $3.92 billion

Why it sold so well: Ultomiris, developed by Alexion, AstraZeneca Rare Disease, is emerging as a hematology drug to watch in 2025, driven by strong commercial momentum and expanding clinical uptake in 2024. The drug generated approximately $3.92 billion in global sales in 2024, marking a 12% increase year over year. In just the first half of 2024, AstraZeneca reported a 21% expansion in its rare disease portfolio last year, with Ultomiris as a key contributor. The drug’s success is largely attributed to its strategic positioning as a next-generation replacement for Soliris, the company’s earlier complement inhibitor. As Soliris revenues declined due to biosimilar competition and patient transitions last year, Ultomiris captured market share. An important factor behind Ultomiris’ growing appeal is its longer dosing interval — every eight weeks versus every two for Soliris.

48. Orencia (abatacept)

Disease area(s): Immunology

Manufacturer(s): Bristol Myers Squibb

2024 Sales (USD): $3.68 billion

Why it sold so well: Orencia’s global sales of $3.68 billion reflected a 2% increase compared to the previous year. This growth was driven by sustained demand in the US market, where sales reached $2.77 billion, marking a 2% increase. Orencia’s continued success is attributed to its established efficacy in treating moderate to severe rheumatoid arthritis and its expanding use in other autoimmune conditions. The drug’s performance underscores its significant role in Bristol Myers Squibb’s immunology portfolio. However, the company anticipates potential challenges in the coming years due to increasing competition from biosimilars and evolving market dynamics.

49. Tremfya (guselkumab)

Disease area(s): Immunology

Manufacturer(s): Johnson & Johnson

2024 Sales (USD): $3.67 billion

Why it sold so well: J&J’s IL-23 inhibitor Tremfya experienced significant sales growth last year with $3.67 billion in total sales, an increase of 16.6% from 2023. Its growth was largely driven by its expanded indications. The drug received approvals for the treatment of ulcerative colitis in September 2024 and Crohn’s disease in March this year, broadening its application beyond psoriasis and psoriatic arthritis. These new indications contributed to increased adoption among healthcare providers and patients. Additionally, the convenience of Tremfya’s dosing regimen and its favorable safety profile enhanced patient adherence and satisfaction. Overall, these factors solidified Tremfya’s position as a leading therapy in the immunology market.

50. Pomalyst (pomalidomide)

Disease area(s): Oncology/hematology

Manufacturer(s): Bristol Myers Squibb

2024 Sales (USD): $3.55 billion

Why it sold so well: Bristol Myers Squibb’s blood cancer drug Pomalyst netted global sales of $3.55 billion, an increase of 3% from the previous year and accounted for approximately 7.3% of the company’s total revenue of $48.3 billion in 2024. The strong performance was primarily driven by sustained demand in the US, where Pomalyst is a key therapy for relapsed or refractory multiple myeloma. Despite facing generic competition, Pomalyst maintained its market position due to its established efficacy and safety profile. Additionally, the drug’s inclusion in combination therapies contributed to its continued utilization in clinical practice. In April 2025, a federal judge dismissed a proposed class action lawsuit against Bristol Myers Squibb, which alleged the company illegally maintained a monopoly over Pomalyst. The plaintiffs failed to prove that the company and its subsidiary, Celgene, engaged in fraudulent patent practices or filed baseless lawsuits to block generic competition.

Join or login to leave a comment

JOIN LOGIN